Understanding Investment Growth and Compounding

An Investment Growth Calculator helps you estimate how your investments can grow over time based on your initial investment, regular contributions, expected rate of return, and investment duration. By simulating different scenarios, you can better plan your financial goals and understand the potential outcomes of your investment strategy.

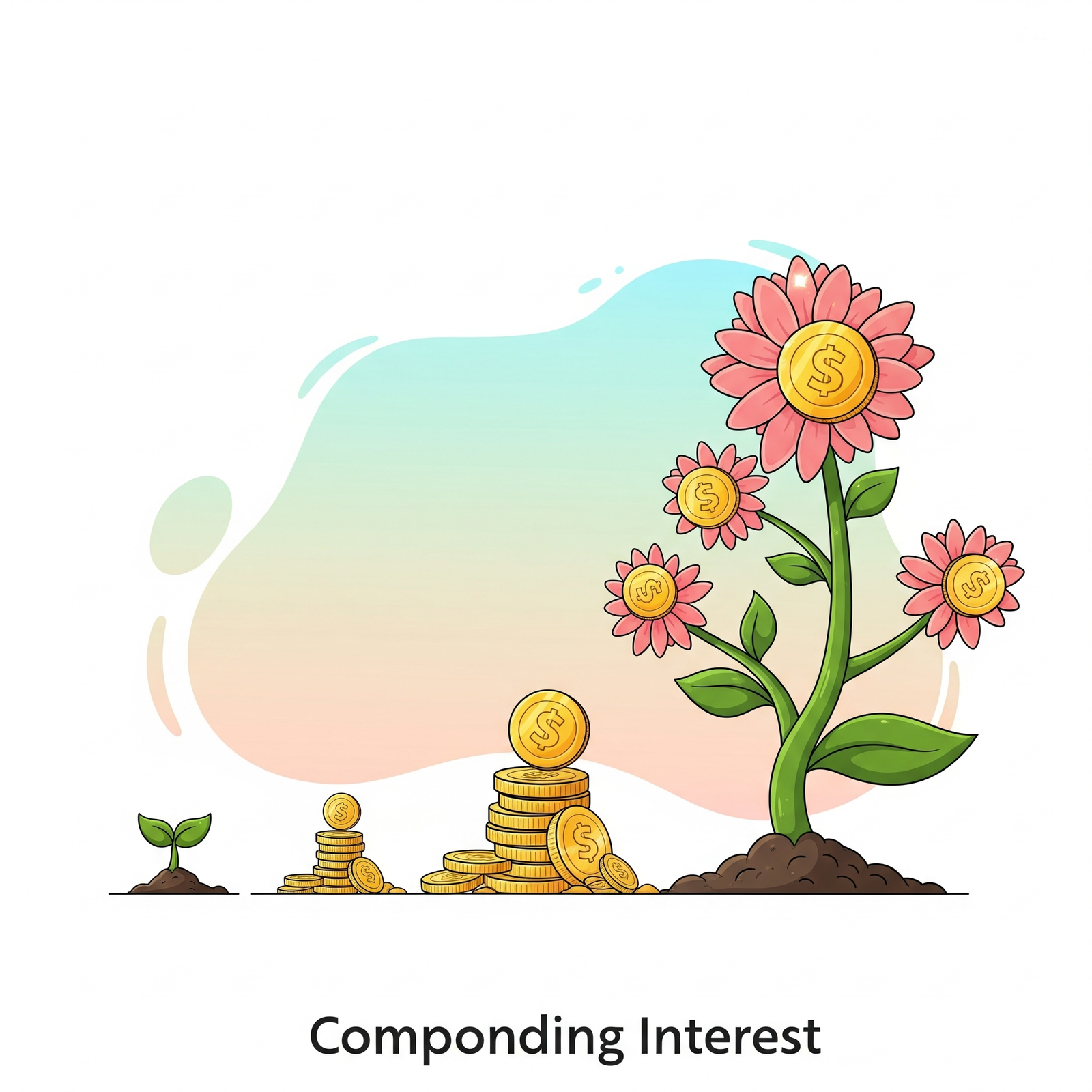

The core principle behind significant investment growth is compounding, often referred to as "interest on interest." This means that not only does your initial investment earn returns, but the returns themselves also start earning returns. Over longer periods, this snowball effect can dramatically increase your wealth, making time a powerful ally in investing.

Visual representation of money compounding over time, leading to significant growth.

Visual representation of money compounding over time, leading to significant growth.

Key Factors Influencing Investment Growth

Several factors play a crucial role in determining how quickly and substantially your investments grow:

- Initial Investment: The starting capital you put in. A larger initial sum generally means a larger base for compounding.

- Regular Contributions: Consistent additions to your investment accelerate growth by adding more capital to earn returns. Even small, regular contributions make a big difference over time.

- Annual Interest Rate (Rate of Return): The percentage at which your investment grows each year. Higher rates generally lead to faster growth, but often come with higher risk.

- Investment Period (Years): The duration your money remains invested. This is perhaps the most critical factor for compounding; the longer the period, the more time your returns have to earn additional returns.

- Inflation: The rate at which prices for goods and services increase. Inflation erodes the purchasing power of your money, so it's important that your investment returns outpace inflation to achieve real growth.

Strategies for Maximizing Investment Returns

While the calculator provides a quantitative estimate, adopting sound investment strategies can help you achieve your financial goals:

1. Start Early and Invest Consistently

The power of compounding is most evident over long periods. Starting early allows your investments more time to grow, and consistent contributions, even modest ones, build up substantial wealth over decades. Time in the market often trumps timing the market.

2. Diversify Your Portfolio

Don't put all your eggs in one basket. Diversification involves spreading your investments across various asset classes (stocks, bonds, real estate), industries, and geographies. This strategy helps reduce risk, as a downturn in one area may be offset by gains in another.

3. Reinvest Earnings

To fully leverage compounding, reinvest any dividends, interest, or capital gains back into your investments. This increases your principal, allowing future returns to be calculated on a larger base.

4. Understand and Manage Risk

Every investment carries some level of risk. Understanding your risk tolerance and aligning it with your investment choices is crucial. Higher potential returns often come with higher risk. A balanced approach involves taking calculated risks while protecting your capital.

Common Investment Types to Consider

There are numerous ways to invest your money, each with different risk-reward profiles:

- Stocks: Represent ownership in a company. High growth potential, but also higher volatility.

- Bonds: Loans made to governments or corporations. Generally lower risk than stocks, providing fixed income.

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other assets. Offer diversification and professional management.

- Exchange-Trald Funds (ETFs): Similar to mutual funds but trade like stocks on exchanges. Often have lower fees.

- Real Estate: Investing in properties directly or through Real Estate Investment Trusts (REITs). Can provide income and appreciation.

- Certificates of Deposit (CDs): Savings accounts that hold a fixed amount of money for a fixed period, offering a fixed interest rate. Low risk.

- Savings Accounts: Basic accounts for holding cash. Low returns, but high liquidity and no risk.

- Retirement Accounts (401(k), IRA): Tax-advantaged accounts designed for long-term savings for retirement.

Visual overview of various investment types to help you diversify your portfolio.

Visual overview of various investment types to help you diversify your portfolio.